Right after the election, I got to speak on The Redress Movement‘s panel about Building Racial Redress Into Housing Justice. They invited me on behalf of my client organization’s homeownership initiative that provides down-payment assistance specifically for first-time buyers who identify as Black and/or Latino… which begs the question, why bother listening to me if programs like ours are about to become “too risky”?

Well… when I took my organizational hat off, it turned out I had a few personal things to say to my fellow white folx in the social sector about how we tend to measure risk. Video is here, and I’ll paste in a transcript of my risk comments below. Strong recommend on watching the other panelists too, if you’ve got the time and interest – there’s a lot of great work happening, and it WILL continue. No matter what.

***

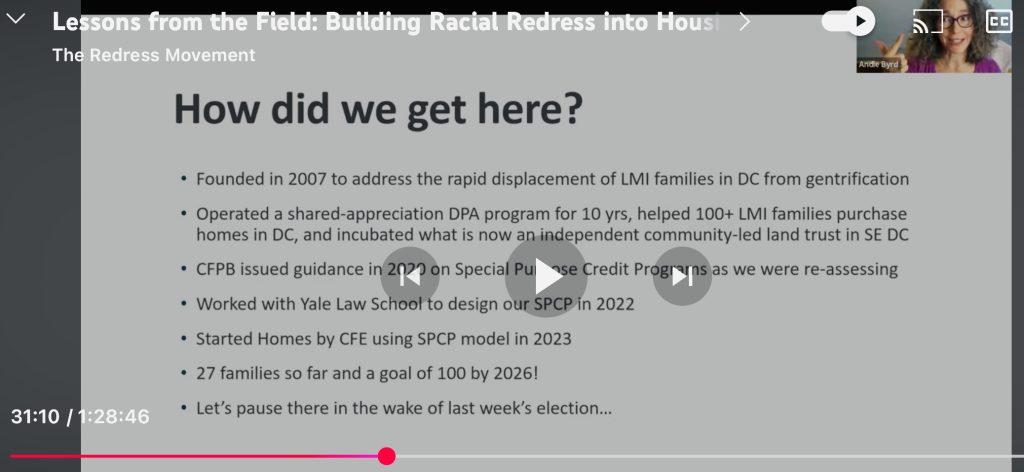

I am going to pause for a sec in the wake of last week’s election, because I just said three things:

I said that we are explicitly race-conscious; we’re using guidance by the CFPB; and that guidance is from 2020, and we all know that the context in which we’re operating has changed. A LOT. It’s changed already, it’s gonna change more.

But here’s the thing. We are operating not just in accordance with justice, we are operating within the law. We are not going to do any fear-based thing of self-censoring or complying in advance of anything that MIGHT happen.

And I’m actually going to take off my official hat and speak from a really personal place for a sec, about how we approach this question of taking risk in our work.

Because really, I feel like some of you might be having this question about, like, “Should I just tune out for like the next 10 or 15 minutes that Andie will be talking because, like, obviously that’s super risky and we’re not gonna be able to do that anymore.”

And so I want to start off by reminding all of us – and especially my fellow white folks – that we can decide to take risks for justice. Right?

The idea that something is risky, doesn’t mean we shouldn’t do it.

Oftentimes, for those of us whose skin color and baseline level of financial security and other lived experiences are like mine – aka people who tend to have more power and privilege in our organizations – we need to ask ourselves the question:

If we don’t take a risk when it’s a matter of justice, who are we assigning that risk to?

Because the risk is still there. It doesn’t go away. It’s just a question of who has to live with it.

If we don’t explicitly confront the reality of racial injustice in mortgage lending – guess who still has to confront it? It’s the same people who always have, right? It’s the same Black and Brown families who for generations have been denied access to the financial system in, like, every possible way.

So if we are sitting within our organizations and we’re having conversations about choosing the safer course, now is the time to make sure that we’re asking: safer for whom?

Because we have responsibilities to our organizations. We have our boards, we have our legal advisors, and some of you are from government agencies and you don’t have a lot of flexibility – cool, there’s lots of voices telling us to be careful, especially now. And I’m not saying that we should break any laws.

I’m just saying that If we personally are not used to that sense of risk, that worry that we might be targeted, we need to recognize WHY we’ve been shielded from it. And then we need to consider, is now the time that I can take on my rightful share of risk in this system as it currently exists?

So, I’m gonna get my organizational hat, I’m gonna put it back on, and I hope that’s a useful frame to keep in mind as we go on.

***

Hope this resonates for you. Onwards, my friends. Always. ![]()